Sometimes bad things happen when you’re a homeowner. Scary things like hail, fire, tornados, acts of God – the long list of dangers you see in your homeowner’s insurance. When something bad happens, the good news is that you probably have some form of insurance! The bad news is that if it’s a Condo Association insurance casualty, things are not as straightforward as they would be in a single family home. These tips will help you navigate a challenging issue.

Immediately Get Your Insurance Involved

Condo Association insurance casualties get complicated quickly. Depending on the cause of the casualty, the state you live in, and the coverage of your Condo master insurance policy and your own policy, there can be multiple outcomes. Remember, your Condo Association Board has a fiduciary duty to the Association – not to you. You need to get your own insurance involved ASAP. Your insurance won’t want to pay a dime more than they have to, and they can fight it out with your Condo Association more effectively than you can. Make sure to get them involved quickly.

Be Patient

There are multiple factors that can lead to a Condo Association insurance casualty taking a long time to resolve. First, the Condo’s insurance must complete an investigation. Upon completion, the findings will be provided to you. If it was a large incident – think hurricane damage or a big fire – it could take some time. Next, the Condo needs to get a repair company on contract. This can take some time. Finally, you need to coordinate the Condo’s activities with your own insurance. Even more time.

It sucks, but don’t expect immediate gratification. Resolving a Condo Association insurance casualty is not a fast process.

Look Out for Yourself

During a Condo Association insurance casualty, all parties are going to be looking out for themselves. Insurance will want to pay as little as possible. The Condo Association will be protecting its own finances. If the incident is large, your Management will have to deal with many units.

Make sure you’re looking out for yourself and following up with everyone you need to constantly. Take nothing for granted. Ask Management, the Board, and your insurance company for regular updates. Don’t assume silence is a good thing. Don’t be rude or obnoxious, but do check in weekly or as is appropriate.

Condo Association Insurance Casualty Issues are Challenging

Dealing with casualty issues is a challenge. Your home is damaged or destroyed, along with your personal belongings. In and of itself, this is an extremely upsetting and disruptive event. Your top priority is going to be getting things back to normal. Make sure you set realistic expectations and stay politely persistent, and you’ll navigate a tough situation and lead a better Condo life.

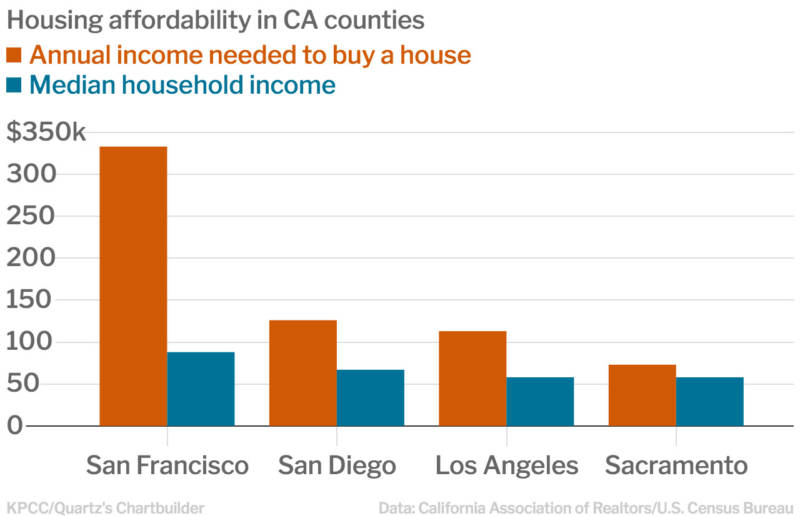

San Jose Realtor Holly Barr sold this burned-out home for more than $900,000. (Matt Levin/CALmatters)Technically, California has seen higher prices before. During the housing boom of the mid 2000s, the median statewide price nearly broke the $600,000 barrier (and that’s without adjusting for inflation). Many parts of California are still cheaper now than they were a decade ago.But Silicon Valley is not one of those places.The median price of a single family home in Santa Clara County — home of Apple and Google — hit $1.4 million in March of this year, according to data from the California Association of Realtors. That’s an all-time high.The region’s housing market has transformed any piece of available land into a veritable gold mine. No matter what sits on top of it.Real estate agent Holly Barr says she’s never had a listing generate as much attention as the one on Bird Avenue in the San Jose neighborhood of Willow Glen. The house caught fire two years ago during a remodeling job. What was left was a burned-out husk of a California bungalow sitting on 5,800 square feet of land.When Barr put the property on the market in April for $800,000, the listing made international headlines. It sold for over $900,000 — in less than a week. The burned down house will be razed and a new property will be built there that will likely sell for far more.“I wasn’t surprised,” said Barr. “It’s not about the house, it’s about the land and location.”It’s also not a surprise that with unliveable wrecks selling for that much, residents are starting to look for other places to live.According to data from the California Department of Finance, Santa Clara County lost 17,000 more residents to other parts of the state or country than they gained last year. That’s the second biggest net domestic migration loss of any county in the state.Los Angeles: A Fixer-Upper, or a House Smaller Than Your Expectations

San Jose Realtor Holly Barr sold this burned-out home for more than $900,000. (Matt Levin/CALmatters)Technically, California has seen higher prices before. During the housing boom of the mid 2000s, the median statewide price nearly broke the $600,000 barrier (and that’s without adjusting for inflation). Many parts of California are still cheaper now than they were a decade ago.But Silicon Valley is not one of those places.The median price of a single family home in Santa Clara County — home of Apple and Google — hit $1.4 million in March of this year, according to data from the California Association of Realtors. That’s an all-time high.The region’s housing market has transformed any piece of available land into a veritable gold mine. No matter what sits on top of it.Real estate agent Holly Barr says she’s never had a listing generate as much attention as the one on Bird Avenue in the San Jose neighborhood of Willow Glen. The house caught fire two years ago during a remodeling job. What was left was a burned-out husk of a California bungalow sitting on 5,800 square feet of land.When Barr put the property on the market in April for $800,000, the listing made international headlines. It sold for over $900,000 — in less than a week. The burned down house will be razed and a new property will be built there that will likely sell for far more.“I wasn’t surprised,” said Barr. “It’s not about the house, it’s about the land and location.”It’s also not a surprise that with unliveable wrecks selling for that much, residents are starting to look for other places to live.According to data from the California Department of Finance, Santa Clara County lost 17,000 more residents to other parts of the state or country than they gained last year. That’s the second biggest net domestic migration loss of any county in the state.Los Angeles: A Fixer-Upper, or a House Smaller Than Your Expectations